The Controllability Principle

The idea of holding managers responsible for those decisions for which they are given authority is called the controllability principle.

Controllable costs are costs affected by a manager’s decisions. Managers affect controllable costs; therefore, these costs partially reveal the actions of the manager.

Through the measurement of controllable costs, superiors have information about what decisions the manager has made; therefore, controllable costs are potential performance measures for the manager who controls those costs.

For example, the manager of a manufacturing plant is held responsible for the plant’s costs because the manager makes decisions that affect plant costing.

A single manager generally does not have control over all of an organization’s costs. Each manager has responsibilities, which are limited by the manager’s job description, and allow the manager to control only certain costs.

Some costs also are affected by the organization’s environmentOpens in new window and not controlled by any managers of the organization. For example, economic forces that a plant manager cannot control affect the cost of raw materials. Uncontrollable costs generally do not reveal the actions of the manager, and are less useful performance measures.

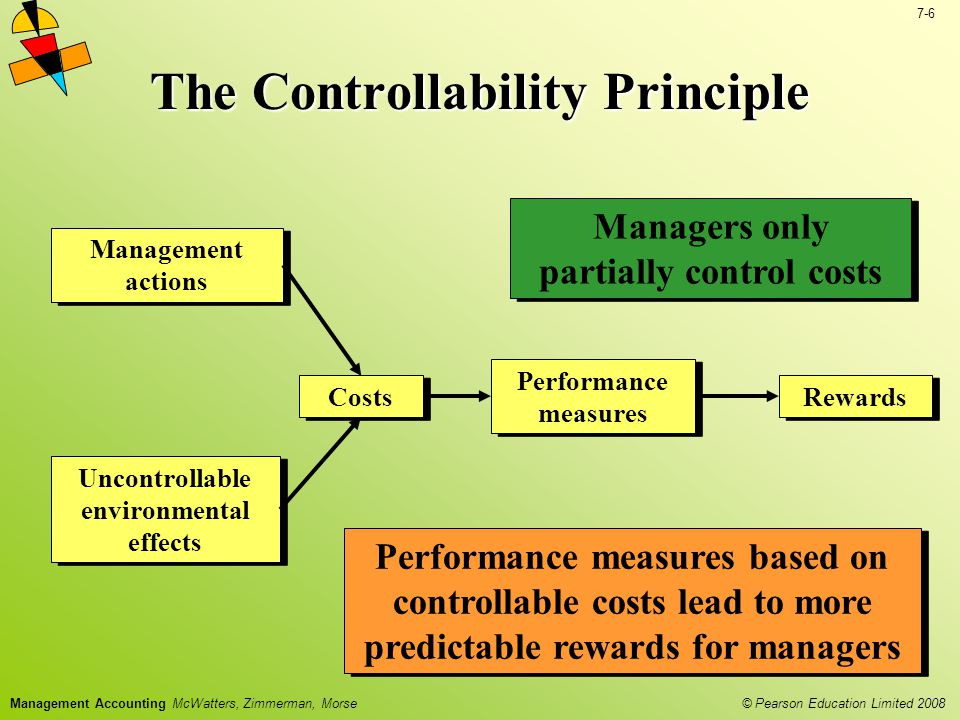

Costs generally cannot be classified as either completely controllable or completely uncontrollable. Figure X1 demonstrates that costs are usually influenced by both managerial actions and uncontrollable environmental factors.

For example, if a yacht-club manager is not held accountable for damage done by hurricanes, the manager has less incentive to prepare the yacht club for severe storms.

Figure XI, Controllability of cost

Figure XI, Controllability of cost

|

While managers cannot influence the likelihood of hurricanes, they can influence the costs incurred from the impact of severe weather. Along with taking steps to safeguard the yacht club, the manager can obtain insurance to mitigate the financial impact of damages.

In these cases, the manager should be responsible for the portion of costs that can be controlled. Holding managers accountable for only those costs solely under their control does not provide them with incentives to take actions that can affect the consequences of an uncontrollable event.

The feedback loop from the performance measure and rewards in Figure 1X demonstrates the influence of the performance measurement system and the reward system on the actions of the manager.

Managers prefer to be evaluated based on controllable costs as it makes their rewards much more predictable. Managers generally do not want their rewards to be uncertain. To avoid uncertainty, managers do not want performance measures that are affected by factors they cannot control. Therefore, controllable performance measures, such as controllable costs, are preferred performance measures.

Some performance measures, however, are partially affected by factors not under the manager’s control. In the previous example, hurricanes were not controllable, but hurricanes affected costs. Managers would like to eliminate the uncontrollable portion of the costs from their performance measures.

One method of removing uncontrollable factors from a performance measure is to compare performance measures of different managers facing similar circumstances.

With relative performance measurement, the performance of a manager is judged relative to the performance of a comparison group.

The comparison group helps control for random events that affect both the person being evaluated and the comparison group.

If the costs of the yacht-club manager are compared with those of other yacht-club managers adversely affected by the hurricane, the uncontrollable effects of the hurricane can be eliminated.

Relative performance measure is also used in assigning course grades. Many instructors ‘curve’ the grades. Instead of awarding A grades for scores of 85 to 100, the top 10 percent of the class receive As. Curving the grades controls for unusually easy or hard exams, and is a way to remove some of the risk for students.

Relative performance measures, however, do not recognize whether all the students or managers performed better or worse than some absolute standard. By comparing individual performances with the performance of others, approximately half of the individuals will always be graded better than average and half will be graded worse than average.

No possibility exists for all individuals to be rated above average, even if all the individuals performed their duties as specified. Relative performance measures discourage co-operative effort, because individuals recognize that they will be compared with the other individuals.

In summary, each manager in an organization is given certain responsibilities. These responsibilities define the limits of the manager’s control. The part of the organization within these limits is under the control of the manager. Ideally, managers are evaluated based on performance measures of activities that they also control.

You Might Also Like:

- Research data for this work have been adapted from the manual:

- Managerial Accounting: Tools for Business Decision Making By Jerry J. Weygandt, Paul D. Kimmel, Donald E. Kieso